takes on...

takes on...

I am a little disappointed in the news of new regulations for securitization markets. This article from Dow Jones details the plan that the government will require the firms that securitize debt to hold onto 5% of the securities.

The reason why I'm disappointed is that this is not a change in the status quo. The mortgage securitization shops used to hold onto some of their securities because they couldn't sell them. The securities were so worthless they could not find anyone to buy them, so they kept them. After a long enough period of time, these worthless securities built up, and eventually bankrupted these shops. Here are two examples from one of my favorite bankrupt mortgage securitization shops, Novastar:

What I'm noting from these articles is that these companies always held on to some of their securitizations because they could not sell all of them. Requiring these shops to hold onto a small percentage of their securitizations is NOT a change for the better; it is not a change AT ALL!

Wednesday, June 17, 2009

Friday, June 12, 2009

New Nuclear Fuel

Many analysts have predicted a future shortage of Uranium. Some rumors on the net and in the broadcast media say that known reserves of Uranium will only last 50 years at current usage rates. For this reason, many commodity traders and speculators have been bullish on Uranium in recent years. The spike in new reactor permits would tend to lend credibility to their arguments. Increased demand with limited supply will lead to higher prices.

So, how high can it really go? The beautiful thing about free markets is that they are self-correcting. High prices are the cure for high prices. As the price for Uranium increases, there is a price that is high enough that it is no longer economical to produce electricity. For example, it might be cheaper to produce your power from wind, solar, oil or natural gas, depending on their prices. The situation is a little more complicated than a single supply & demand curve. Now, factor in nuclear fuel pre-processing, safety and nuclear proliferation issues, and nuclear waste concerns, and you’ve found yourself in a big mess.

However, there is a substitute for Uranium. Thorium is a similar element that can also be used to produce nuclear power. It is easier to process into fuel, safer to operate, easier to dispose of, and is much more abundant on Earth than Uranium. The Thorium fuel cycle also does not produce Plutonium 239, which is used to make nuclear bombs. It really is a much better source of nuclear fuel. That is why modern nuclear “Generation IV” reactor designs are built to run on Thorium, NOT Uranium.

I could only find one stock ticker to buy into the Thorium future: THPW. Might make for a good investment. Make sure to read up on the company at http://www.thoriumpower.com.

So, how high can it really go? The beautiful thing about free markets is that they are self-correcting. High prices are the cure for high prices. As the price for Uranium increases, there is a price that is high enough that it is no longer economical to produce electricity. For example, it might be cheaper to produce your power from wind, solar, oil or natural gas, depending on their prices. The situation is a little more complicated than a single supply & demand curve. Now, factor in nuclear fuel pre-processing, safety and nuclear proliferation issues, and nuclear waste concerns, and you’ve found yourself in a big mess.

However, there is a substitute for Uranium. Thorium is a similar element that can also be used to produce nuclear power. It is easier to process into fuel, safer to operate, easier to dispose of, and is much more abundant on Earth than Uranium. The Thorium fuel cycle also does not produce Plutonium 239, which is used to make nuclear bombs. It really is a much better source of nuclear fuel. That is why modern nuclear “Generation IV” reactor designs are built to run on Thorium, NOT Uranium.

I could only find one stock ticker to buy into the Thorium future: THPW. Might make for a good investment. Make sure to read up on the company at http://www.thoriumpower.com.

Wednesday, March 25, 2009

Bailout?

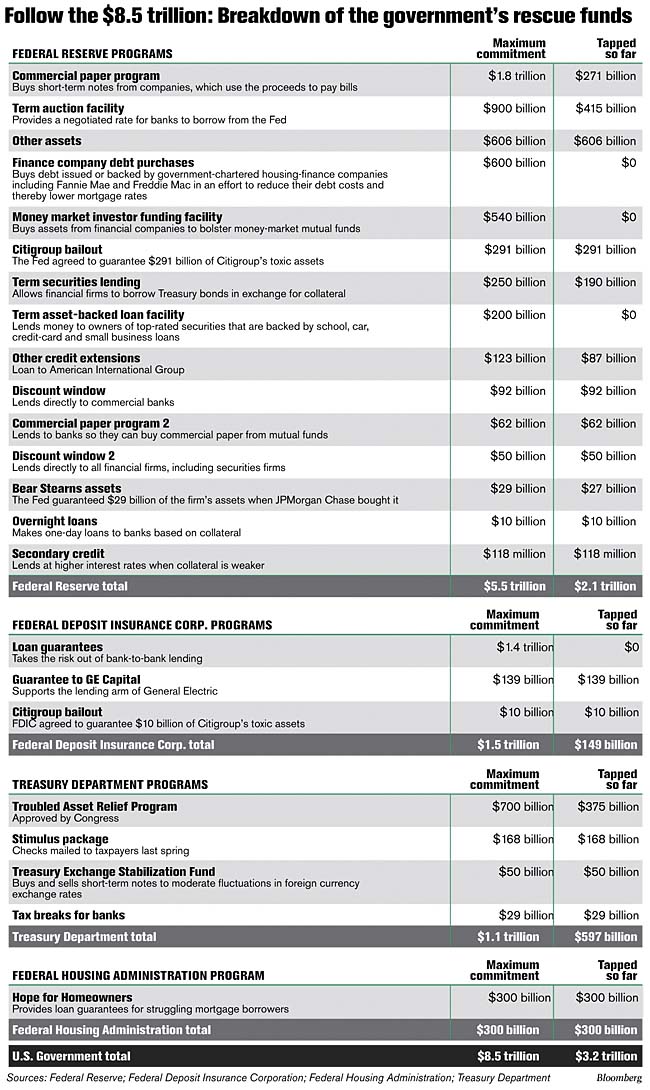

I'm a little upset by all of the bailout programs coming out of Washington. I can't keep track anymore. There is the TARP and the TALF, the two stimulus packages, numerous bailouts for banks, Bear and AIG, and the purchasing of Treasuries by the Fed. A trillion here, a trillion there... Some place total spending estimates now at $8.5 trillion! Here is one count by The Centre for Research on Globalization.

Now, I have said before that I like these programs. I think this is what the government should be doing. However, I do not believe that this problem is one that we can just throw money at. These toxic assets are considered toxic for a reason. Most were created by physicists and mathematicians to be very complex, dynamic securities with many complexities that make valuing them very difficult. They used a mix of dynamic traunching and derivatives like swaps to hedge away risks in the loan portfolios. (Which only work when the counter parties are solvent!) This article gives a good idea of the complexity of these instruments. Valuing these toxic assets continues to be an issue, as it was with the first bailout, when members of Congress grilled Ben Bernanke on how the government could value these assests better than the market can.

I believe that this issue is at the core of the credit crisis. Any plan to fix the credit crisis without dealing with this problem is a waste of time and money. Some of these structured products are so complex that I believe the only solution is to purchase them back from their holders, restructure them, and return them to the owner. This process will remove the complexities of the securities so that individuals can see what they are, rate them accordingly, and value them properly.

What I'm suggesting is no easy task. But this must be done to obtain clarity on what loans underlie these complex securities. Only after we have clarity on these loans can we then move to discussions on mark to market accounting and the like. For more details on exactly what I'm talking about, I recommend this book

Now, I have said before that I like these programs. I think this is what the government should be doing. However, I do not believe that this problem is one that we can just throw money at. These toxic assets are considered toxic for a reason. Most were created by physicists and mathematicians to be very complex, dynamic securities with many complexities that make valuing them very difficult. They used a mix of dynamic traunching and derivatives like swaps to hedge away risks in the loan portfolios. (Which only work when the counter parties are solvent!) This article gives a good idea of the complexity of these instruments. Valuing these toxic assets continues to be an issue, as it was with the first bailout, when members of Congress grilled Ben Bernanke on how the government could value these assests better than the market can.

I believe that this issue is at the core of the credit crisis. Any plan to fix the credit crisis without dealing with this problem is a waste of time and money. Some of these structured products are so complex that I believe the only solution is to purchase them back from their holders, restructure them, and return them to the owner. This process will remove the complexities of the securities so that individuals can see what they are, rate them accordingly, and value them properly.

What I'm suggesting is no easy task. But this must be done to obtain clarity on what loans underlie these complex securities. Only after we have clarity on these loans can we then move to discussions on mark to market accounting and the like. For more details on exactly what I'm talking about, I recommend this book

Friday, February 6, 2009

Pairs Trading Can Be Risky!

So, I thought I’d check up on a pairs trade that I was considering entering last March. Pairs trading involves taking advantage of a correlation between two markets or stocks. When the pairs diverge, you short the higher one and buy the lower one, hoping that they will come back together in the future, and you will capture the difference as profit.

I noted one such divergence between the oil market and the clean energy sector. They usually are highly correlated because higher oil prices makes investment in alternative energy technologies more attractive. Early last year, as oil went on its historic bull run, the correlation broke down. I saw an opportunity for a pairs trade emerge. The chart below shows the divergence:

(from Yahoo Finance)

(from Yahoo Finance)Looking deeper into the pair, the correlation coefficient is 0.49, which is quite a bit lower than the 0.70 that some people consider a minimum for a significant correlation. However, I like the logical argument behind the correlation and attribute the low coefficient to my small data set that only goes back to 2006.

The point of this article is that, sometimes, markets can irrationally diverge for longer than you can stay solvent. Even a hedged pairs trade can be very risky under leverage. But, if you’re careful and patient, you can make money in a logical way!

Tuesday, February 3, 2009

GDP Growth? Or Not?

The way that GDP is reported by our government always frustrated me. The calculation of GDP includes government spending. What this means is that it's possible for the government to borrow money and "create" GDP out of thin air. This is why fiscal policy is so important to the economy.

So, does the government influence GDP with fiscal policy? Of course. I'd like to focus on the most recent Bush administration. During the last 8 years, the economy grew at a small but pretty even rate. However, at the same time, we ran record deficits. So, did the Bush administration create a growing GDP by borrowing money on the

The graph above shows 3 lines. The blue line is the official reported GDP adjusted for inflation. The red line is the government account deficit/surplus. If the red line is above zero, then the government ran a surplus. If the red line is below zero, the government ran a deficit. The green line is GDP minus the government account deficit.

Note that when the government runs a deficit, corrected GDP is lower than reported GDP, because the government is borrowing money to stimulate the economy. When the government runs a surplus, the corrected GDP is higher, because the government is taking money out of the economy, via taxes, and paying off government debt instead of stimulating the economy.

There are some interesting things to note. During the late nineties, the economy was roaring on its own, as much as seven percent, while fiscal policy was paying off government debt. This would tend to show the

I should hope that Obama can learn from what is shown here, and implement sound economic policies that grow the economy, rather than deficit spending to cover up a bad GDP.

Friday, January 30, 2009

Correlation between VIX and Gold?

Some consider the VIX index as a measure of "market fear." Indeed, the index does depend on demand for S&P 500 puts, which is a good sign that portfolio managers are worried about a market drop. I have been thinking recently that gold is another measure of "market fear." When people become concerned about the economy and the solvency of the federal government (along with inflation), they buy gold.

So, we should be able to see a correlation between the VIX and gold, right?

Let's look into it. I'll plot the daily closing value of Gold on the vertical axis and the daily closing value of the VIX on the horizontal axis. My data set goes back to 1991 and contains over 4,000 data points.

What an interesting pattern we see here! I have to say, it does not look like what I was thinking it would look like. The only re-assuring aspects of the graph are the points in the top right (when gold is high, the VIX is high, signaling a correlation) and the points in the bottom left (gold is low, VIX is low, signaling a correlation). Most of the other points, however, do not signal a correlation.

One might argue that Gold is influenced by inflation, while the VIX is not. That would be a good argument. Here is the same graph with the gold price adjusted for inflation using the GDP deflator:

Not as much of a change as we would like. I still find this graph to be very interesting and hope others might be able to comment on it’s value…

So, we should be able to see a correlation between the VIX and gold, right?

Let's look into it. I'll plot the daily closing value of Gold on the vertical axis and the daily closing value of the VIX on the horizontal axis. My data set goes back to 1991 and contains over 4,000 data points.

What an interesting pattern we see here! I have to say, it does not look like what I was thinking it would look like. The only re-assuring aspects of the graph are the points in the top right (when gold is high, the VIX is high, signaling a correlation) and the points in the bottom left (gold is low, VIX is low, signaling a correlation). Most of the other points, however, do not signal a correlation.

One might argue that Gold is influenced by inflation, while the VIX is not. That would be a good argument. Here is the same graph with the gold price adjusted for inflation using the GDP deflator:

Not as much of a change as we would like. I still find this graph to be very interesting and hope others might be able to comment on it’s value…

Thursday, January 15, 2009

Buy Treasuries?

I really am having a hard time understanding some of these "experts" giving advice on where to put your money. Here's another example. His position is that things are going to get worse. State and Municipal governments are going to have huge budget shortfalls this year and are going to require a bail-out by the federal government. His suggestion is to buy treasuries for safety.

Why, why, why would someone tell you to buy Treasuries right after they describe the huge amounts of debt that the government is going to have to take on? How do problems for state and munis cause a bad stock market? Where's the logic in this advisor's argument?

No one seemed to take note when some pointed out that the federal government could easily lose their AAA status. This article is from Sept 08! Think where we are now, with Obama pushing an $800 billion stimulus.

I've had enough of this "the world is ending" talk. Treasuries have peaked. It's time to sell.

Why, why, why would someone tell you to buy Treasuries right after they describe the huge amounts of debt that the government is going to have to take on? How do problems for state and munis cause a bad stock market? Where's the logic in this advisor's argument?

No one seemed to take note when some pointed out that the federal government could easily lose their AAA status. This article is from Sept 08! Think where we are now, with Obama pushing an $800 billion stimulus.

I've had enough of this "the world is ending" talk. Treasuries have peaked. It's time to sell.

Subscribe to:

Posts (Atom)

{kind=link}